We use secondary market pricing data from reputable UK and international fine wine merchants, allowing us to spot undervalued vintages, top performing wines and to inform our clients about what to buy and when. To that end we have created our own Fair Value metric: using critics’ scores and vintage multipliers we can gauge a wine’s inherent worth, its commercial aspect, and when it might be time to drink or sell. The graphs you see in this report are generated in-house with our proprietary data. We are currently developing our own indices to track the performance of various baskets of wine, including Goedhuis favourites and classic performers.

With this in mind, this report will focus on the following themes and their effects on the market:

• The Burgundy 2021 vintage

• China’s Post-Covid Lockdown Reopening

• The Bordeaux Market’s continued strength

• Rising Interest Rates

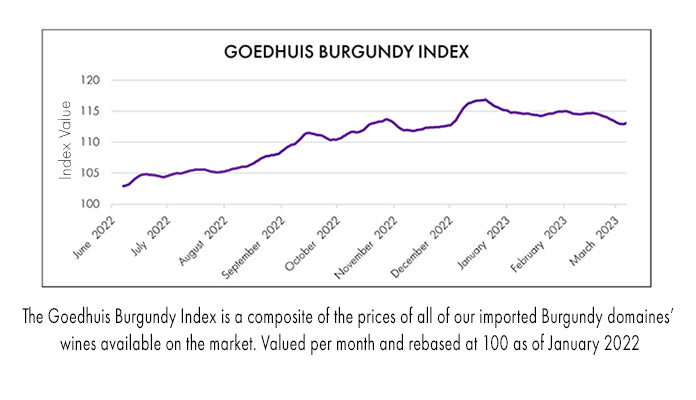

The Burgundy 2021 Vintage

Mother Nature was not kind to the Burgundians in 2021. A combination of early bud-break and a brutal April frost cut yields by 60-80% for the whites, and 50% for the reds. Unusually, Grands and Premiers Crus sites were no better protected against frost than village wines, so even volumes of the top and most sought-after wines were hard hit.

This had a notable impact on the domaines’ release prices, which were up on the 2020 releases by 15-30%. With such a reduced crop, matching last year’s prices was simply not commercially viable. The tiny size of the 2021 harvest was already known last year when the domaines were releasing their 2020s En Primeur, but the price rises for recent vintages have only crystalised in this quarter.

A positive outcome has been a renewed interest in back vintages. Compared to other young vintages, both the 2021s and 2020s are at all-time high prices. However, we have seen much more trade than the macroeconomic conditions would normally indicate; more on this below.

The small size and inherent quality of the vintage ensured the wines sold through, despite the increased prices. The caveat is that Burgundy release prices in general haven’t ever historically dropped. 2022 will be the test vintage, especially as it’s a bumper crop in size.

Ultimately Burgundy’s main strength from an investment perspective has always been small supply outstripped by massive demand and high consumption. With the Asian market and in particular China’s recent reopening, we see that trend continuing.

China’s Post Covid Lockdown Reopening

In response to unprecedented civil unrest in China, the Chinese government lifted their zero-Covid lockdown policy on 7th December 2022.

The macroeconomic talk up until that point had been of long recessions, with indicators such as December’s headline PMI from S&P at 48.2 marking the fifth consecutive month of global contraction. Chinese President Xi Jinping’s policy reversal has proven a catalyst to the global economy, at a time when it was sorely needed. Although it has been a cautious reopening for many businesses, our fine wine sales to Hong Kong and Asia rose 18% on last year, and trade sales to companies selling to Asia are at a four year high.

When the West reopened in early 2022, a huge proportion of unspent funds were funnelled into goods and services. The anticipation of the same from China, whose household savings hit a record $2.6tn at the end of 2022, has led merchants in Hong Kong, Singapore and Seoul to restock. The sales mix here has been a healthy combination of young and mature Bordeaux, Burgundy, Super Tuscans and Champagne. Even though this restocking has been anticipatory, we expect increased trade in Q2, and a more significant renewal of activity in H2 of this year.

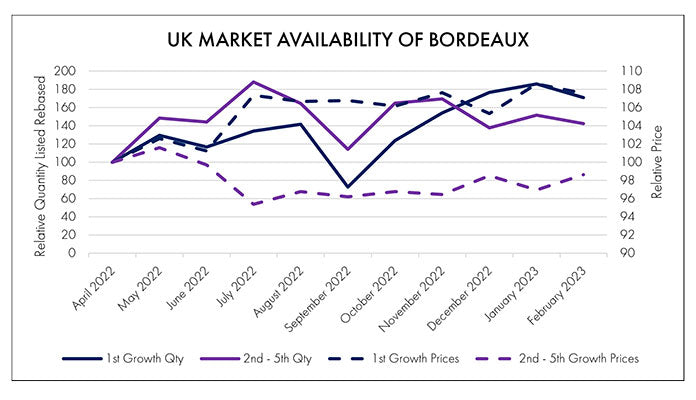

The Bordeaux market’s continued strength

Bordeaux has proven remarkably resilient in the face of the challenging macroeconomic picture. After marginal price declines in H2 2022 as more stock came on to the market, prices have stabilised in Q1 2023, helped both by renewed interest from Asia and from Bordeaux La Place itself. The belief that stock is king still reigns in Bordeaux, especially after the bumper year of ex-château releases in 2022.

As you can see from our in-house data, despite the increased availability in the market, First Growth prices for young vintages (2010-2019) have risen slightly this year having plateaued for most of 2022. The prices of those of the same age in the Second-Fifth Growth bracket have remained steady. Fundamentally, despite the large volumes produced compared to other regions, Bordeaux still represents the benchmark of quality and ability to mature against which all other regions are measured.

Bordeaux activity in Q1, which is traditionally a Burgundy focussed quarter, was also helped by several retrospective and in-bottle tastings by the critics. Key UK wine critics retasted the 2019s in bottle at the annual Southwold Tasting in February, resulting in several surprises. Goedhuis Buying Director, David Roberts MW, highlighted Châteaux Cantemerle, Montrose and La Conseillante as his standouts from their flights. February also brought in-bottle reviews from Vinous’ Neal Martin and Antonio Galloni and The Wine Independent’s Lisa Perrotti-Brown, all three giving perfect scores to Right Bank wines such as Chateaux Angelus, Ausone, Canon, Cheval Blanc, and Trotanoy, encouraging renewed interest in the newest physically available vintage.

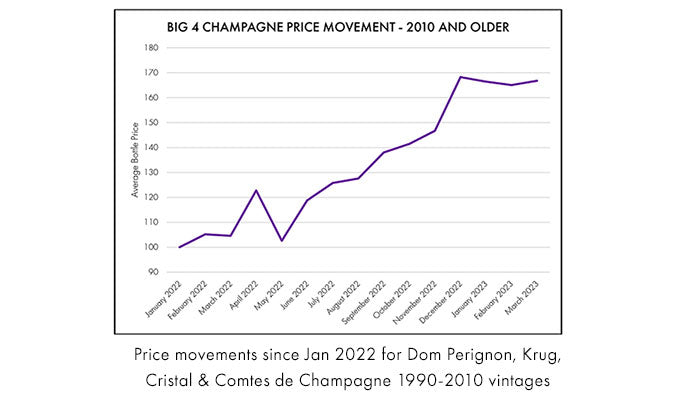

Rising Interest Rates

The end of the global ZIRP (Zero Interest Rate Policy), has been welcomed by many observers as needed for a healthy, functioning economy. However, its ramifications are only just beginning to be felt.

The policies enacted to combat high inflation in H2 2022 led some investors to realise their fine wine gains, while others needed to liquidate their assets to pay for increased costs related to higher interest rates. We have seen this borne out with plateauing Champagne prices this Q1, as despite the bull run of the past 18 months, there has been an influx of back-vintage of stock onto the market.

This increased availability of stock has not, however, caused prices to decline, as the strong demand from those buyers who weren’t able to secure an original allocation has kept the market stable. With the previously mentioned dearth of stellar vintages on the horizon, we expect mature Champagne prices to hold in the short term and increase further over the mid to long term.

Looking Ahead to Q2

Q2 is invariably one of our busiest quarters. Our specific focus will be on the themes of Bordeaux En Primeur 2022, the evolving Grower Champagne market and Italy’s resurgence, including Ornellaia’s new releases.

Bordeaux En Primeur 2022

Unlike this time last year, the châteaux and the negociants have been singing the praises of the forthcoming Bordeaux vintage. Despite drought-like conditions in 2022, with the driest summer on record since 1959, and a shorter harvest period for many properties, the quality of the grapes is high, albeit with lower yields due to smaller berries.

The likely upshot is that given a small vintage, similar to 2021, we will see the chateaux maintaining last year’s prices at a minimum, unless the global macroeconomic picture deteriorates materially. We are very much looking forward to heading out to taste the wines in barrel in the last week of April, and will report back our findings before the commencement of the campaign itself in May.

The Grower Champagne Market

With the smart money looking for other undervalued regions and wines with similar potential to Champagne’s recent bull run, prominent voices have been pointing to Grower Champagnes as potential candidates.

Unlike most other major wine regions, Champagne is highly fragmented, with vineyards owned by multiple smaller farmers, many of whom have contracts with the bigger houses to supply grapes. Unsurprisingly, some ambitious and quality focused growers also make their own Champagne in-house.

By law, Champagne’s governing body requires that these producers put RM (Récoltant-Manipulant) on their bottles, designating a grower who makes Champagne from grapes grown in their own vineyards and produced on their own premises. An RM is not allowed to purchase more than 5% of the fruit that they process.

The best known RM, Domaine Jacques Selosse, was originally founded in 1949. Today it is run by Jacques’ son Anselme, who did internships at Domaines Coche-Dury, Comtes Lafon and Anne-Claude Leflaive. The similarities with Burgundy are not coincidental, as the vineyards are classified in the same way, and the shared ownership likewise.

Two other renowned RMs are Montagne de Reims based Egly-Ouriet and Ulysse Colin in Côte des Blancs. This is an emerging category within the broader Champagne segment and we look forward to following this area with excitement.

ITALY'S RESURGENCE

The market’s interest in Italy has once again returned courtesy of a multitude of strong vintages for Italy’s top fine wine producing regions.

In the words of Antonio Galloni, “Barolo bounces back with a stellar vintage in 2019 that could very well represent the beginning of a new cycle of strong, outstanding years for this historic appellation. The 2019s are potent, tightly wound wines that will thrill readers who appreciate the nuance, subtlety and structure of Nebbiolo”.

Meanwhile in Tuscany, according to Vinous’ Eric Guido, “At the top level, many of the 2018 Brunellos come across as quite Burgundian in nature, where a combination of vividly dark, ripe fruit, balanced acidity and refined tannins add a brilliant dimension that shines already today”. We’re very much looking forward to offering Gianni Brunelli, Biondi Santi and Gaja’s Pieve Santa Restituta.

Lastly, the Super Tuscans have been releasing their 2020s to great acclaim. We were extremely pleased to offer our partner Ornellaia’s new releases earlier this week. The major critics are enthralled, with Matthew Jukes awarding a perfect 20+/20 for the first time, and The Wine Advocate’s Monica Larner awarding 95-97 points, declaring: “This broad and generous expression has a beautiful quality of fruit and oak that speaks to the very best of Italian winemaking.”

Also not to be missed is their brilliant drinking wine Le Volte dell'Ornellaia 2021. This younger sibling of Super Tuscan royalty has become a superstar in its own right and is always one of the top value Italian buys of the 2021 vintage.

Closing Thoughts – Fine Wine in a high interest rate environment

Since the middle of 2008 global interest rates have been at rock bottom, and in some instances even turned negative. This has meant that for assets in general, and fine wine specifically, the cost of carry has been extremely cheap. Business models which rely on stockholding have consequently chosen to build up large positions. Nowhere is this more the case than the negociants in Bordeaux.

In more expensive and less in-demand vintages like 2017 and 2021, châteaux have been able to maintain their higher prices, as negociants will take all they are offered to retain their allocations. In more sought-after years like 2016 and 2020, the negociants have taken extra stock with a view to future sale at higher prices.

From a consumer’s point of view, the new higher interest rate regime is likely to mean that over the coming years there will be push-back from negociants who aren’t in a position to take every allocation that they are offered. By extension, this will lead to more conservative price-rises from the châteaux, as well as increased availability of well-priced parcels of mature stock from negociants.

The positive outlook from an investment perspective is that new releases will have to give buyers more potential upside than has been the case over the past decade where the châteaux have fully priced wines, taking all of the price-growth potential.